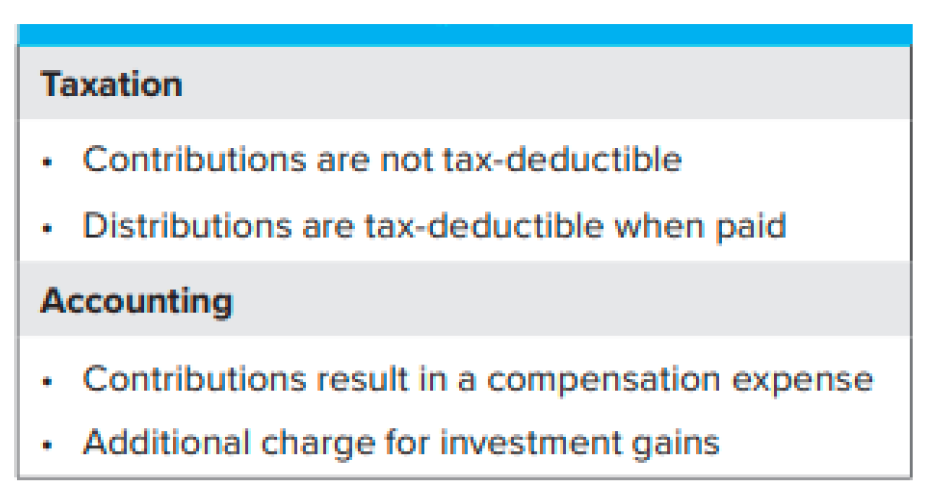

Employer – Compensation is not deductible when deferred. FICA and Medicare taxes are payable when compensation is deferred or employer contributions vest. Benefits are deductible when paid. Gains on trust assets are taxable to the corporation in the same manner as if held directly by the corporation.

Employee – FICA and Medicare taxes are payable when compensation is deferred or employer contributions vest. Employee is not subject to income tax until distribution. Income from the plan is taxed as ordinary income. Distributions are not subject to FICA and Medicare taxes to the extent they were previously subject to such taxes.

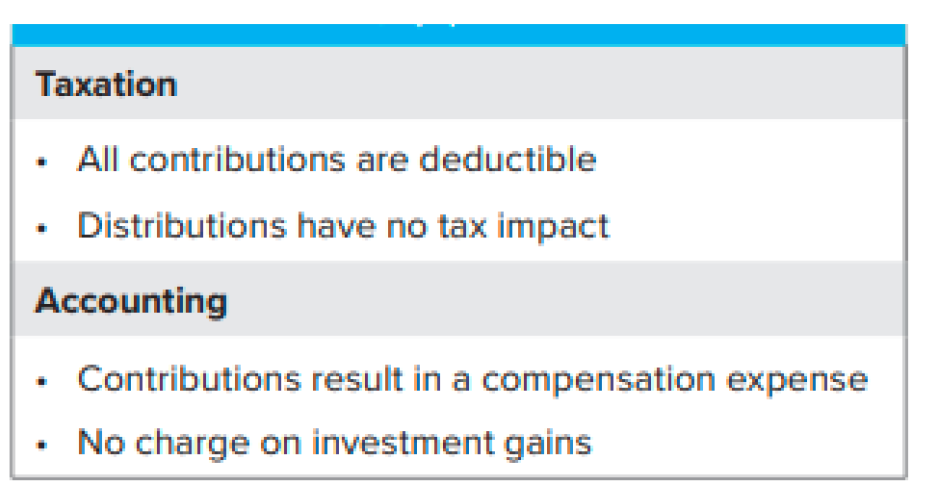

401(K)

NQDC