For a number of years I have worked with community banks designing executive and director retirement programs, as well as Bank Owned Life Insurance (BOLI) investment portfolios. While each program is unique and specifically catered to meet a bank’s individualized needs and strategic goals, one potentially beneficial but often overlooked approach is a Nonqualified Deferred Compensation Plan (NQDC).

A NQDC plan is similar to a 401(k) plan, in theory, as it allows compensation to be saved both pretax and tax deferred until a later date. Section 409A of the Internal Revenue Code regulates the tax treatment for nonqualified deferred compensation programs. The two primary requirements under 409A are that an executive must elect to defer the income prior to earning it and defer it until a specific date or age. The executive also must decide the form of payment when it is ultimately paid. Form of payment refers to the participant being paid via a lump sum or paid over a period of time.

A major NQDC plan difference in comparison to a 401(k) plan is that any amount deferred is subject to creditors of the bank until they are paid out. This can sometimes be a stumbling block for smaller privately held corporations looking to offer a nonqualified deferred compensation program but this is much less of an issue with community banks since community banks have long histories and strong balance sheets due to ongoing regulatory scrutiny and troubled banks are most likely to merge with another bank as an exit strategy rather than fail.

Due to the ever increasing tax rate environment, deferral of income from a savings perspective can be a very meaningful benefit, especially for individuals in higher tax brackets. NQDC plans are flexible and can be structured on a voluntary basis where the employee voluntarily contributes a portion of their pay, employer paid or a combination of both.

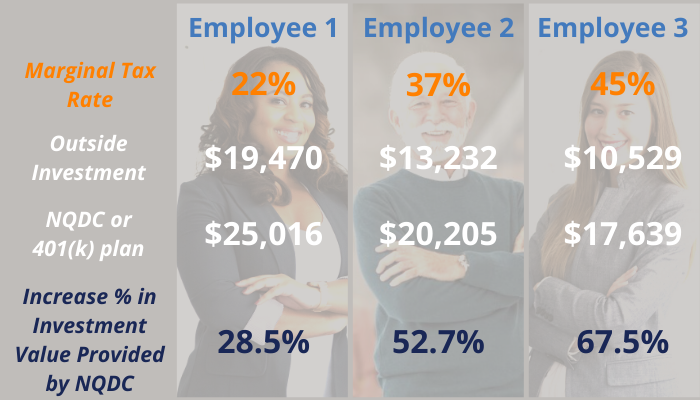

To illustrate, three employees have marginal tax rates of:

- 22% (third lowest federal tax bracket, applicable to those with taxable income between approximately $38,700 and $82,499),

- 37% (the highest federal income tax bracket), and

- 45% (a tax bracket many highly compensated employees may fall into).

Each employee splits $20,000 evenly between two investment vehicles:

- An outside investment that is fully subject to ordinary income taxes, or

- Their employer’s NQDC (or 401(k) plan)

For simplicity, we will assume the outside investment and the employer plan both earn pretax annual rates of return of 6% and the employees’ marginal tax brackets remain the same in all years.

While each employee substantially benefits from deferring the payment of taxes, the value of the tax deferral increases significantly for the two highest tax bracket employees. The opportunity cost to these highly compensated employees of not taking advantage of their tax deferral opportunities can be quite high.

A NQDC plan is a valuable savings vehicle for top earners and it is a proven reward and retention device for employers. Competition for top talent is increasing as the economy improves and keeping key employees is critical to a bank’s long-term success. Key employees are a valuable entity to an organization but also a prized target for competitors. Voluntary contributions into a NQDC plan offers a valuable tool for future savings and if a bank’s peers don’t offer a similar program, the plan participants are less likely to leave.

Another way to add a retentive quality to these plans is to utilize them in conjunction with the bank’s other executive rewards programs. For banks placing greater emphasis on incentive compensation, the bank can pay a portion of an executive’s reward directly into a NQDC plan which is subject to vesting requirements and thus leaves something at risk for a top executive that might be considering leaving the bank.

As an example, I recently worked with a bank that paid 50% of incentive compensation payments into their nonqualified deferred compensation program. The plan had a five year rolling vesting schedule, with each contribution having its own vesting terms, allowing executives to either take the payment once fully vested or defer until termination or retirement. The result was that many executives had approximately $150,000 of unvested dollars in the NQDC plan. This is a significant amount of money to simply walk away from should another opportunity arise.

For executives in leadership positions where a high level of their compensation is incentive based, this type of program performs quite well. It also allows the bank to provide a higher level of compensation knowing there is a solid retention element in place.

NQDC is a widely used strategy in corporate America that is being overlooked in the banking industry. It may not be the right fit for every bank, but because it provides a unique savings tool and proven retention qualities for key employees, it’s certainly worth exploring.

Disclaimer

This information is for general and educational purposes and not intended as legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Information obtained from third-party sources are believed to be reliable but not guaranteed. The tax and legal references attached herein are designed to provide accurate and authoritative information with regard to the subject matter covered and are provided with the understanding that BoliColi.com is not engaged in rendering tax, legal, or actuarial services. If tax, legal, or actuarial advice is required, you should consult your accountant, attorney, or actuary. BoliColi.com does not replace those advisors. Securities and Investment Advisory Services Offered Through M Holdings Securities, Inc. A Registered Broker/Dealer and Investment Adviser, Member FINRA/SIPC. BoliColi.com is independently owned and operated. File # 4869791.1